Your credit score is a three-digit number that can save you — or cost you — tens of thousands of dollars over your lifetime. It affects your mortgage rate, car loan terms, apartment applications, and even job offers. Understanding how it works is the first step to taking control of it.

What Is a Credit Score?

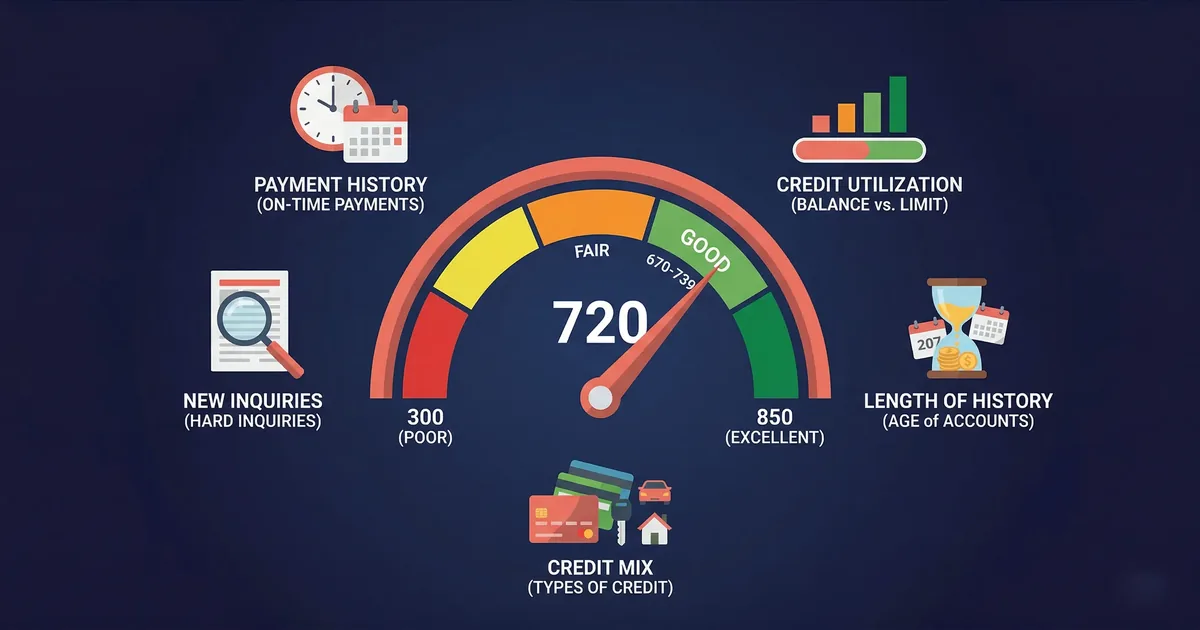

A credit score is a number that shows how likely you are to repay debt. It is based on your credit history. Lenders use it to decide whether to lend you money. The most widely used model is the FICO Score, ranging from 300 to 850.

Three major credit bureaus compile your credit data: Equifax, Experian, and TransUnion. Your score may differ slightly across bureaus because not all creditors report to all three.

Credit Score Ranges

| Score Range | Rating | What It Means |

|---|---|---|

| 800–850 | Exceptional | Best rates and terms available |

| 740–799 | Very Good | Above-average rates from most lenders |

| 670–739 | Good | Acceptable to most lenders |

| 580–669 | Fair | Subprime rates, limited options |

| 300–579 | Poor | Difficulty getting approved, high rates |

5 Factors That Determine Your Score

| Factor | Weight | What It Measures |

|---|---|---|

| Payment History | 35% | On-time vs. late payments |

| Credit Utilization | 30% | How much of your available credit you use |

| Length of Credit History | 15% | Age of your oldest and average accounts |

| Credit Mix | 10% | Variety of credit types (cards, loans, mortgage) |

| New Credit | 10% | Recent applications and hard inquiries |

8 Ways to Improve Your Credit Score

1. Pay Every Bill on Time

Payment history is 35% of your score. Set up autopay for at least the minimum payment on every account. A single 30-day late payment can drop your score by 60–100 points.

2. Keep Credit Utilization Below 30%

If you have a $10,000 credit limit, keep your total balance below $3,000. Below 10% is even better. Pay down balances before the statement closing date for the fastest improvement.

3. Don't Close Old Credit Cards

Closing cards shortens your average account age and reduces your available credit. Both of these can lower your score. Keep old cards open even if you rarely use them.

4. Limit Hard Inquiries

Each credit application causes a hard inquiry that can drop your score by 5–10 points. Space out applications and avoid applying for credit you do not need.

5. Become an Authorized User

A family member with excellent credit can add you as an authorized user on their card. Their payment history and credit limit may then boost your score. You do not need to use the card.

6. Dispute Errors on Your Report

About 1 in 5 credit reports contain errors. Get your free reports at AnnualCreditReport.com and report any errors directly to the credit bureaus.

7. Diversify Your Credit Mix

Having a mix of credit types (credit cards, installment loans, mortgage) shows lenders you can manage different kinds of debt. Do not open accounts just for the mix — let it happen naturally.

8. Use a Budget to Avoid Overspending

Overspending leads to high balances and missed payments. Track spending with Budgeting365 to stay within your means.

Credit Score Myths

- “Checking my score hurts it.” False. Soft inquiries (checking your own score) have zero impact.

- “Carrying a balance improves my score.” False. You never need to carry a balance. Pay in full each month.

- “Closing cards improves my score.” Usually false. It reduces available credit and can increase utilization.

- “Income affects my score.” False. Income is not a factor in credit scoring models.

- “All debt is bad for my score.” False. Responsible use of credit (paying on time, low utilization) builds a strong score.

Budget Your Way to Better Credit

A good budget prevents missed payments and high utilization. Track your spending with Budgeting365 — free and offline.

Download Budgeting365 — FreeFrequently Asked Questions

What is a good credit score?

670–739 is good, 740–799 is very good, and 800+ is exceptional. Most lenders offer the best rates above 740.

How often does my credit score update?

Every 30–45 days as creditors report to the bureaus on their own schedules.

Does checking my own credit score hurt it?

No. Self-checks are soft inquiries with zero impact.

How long does it take to improve a credit score?

Lowering utilization improves your score in 1–2 billing cycles. Recovering from late payments takes 6–12 months. Rebuilding from bankruptcy takes 2–4 years.

What hurts your credit score the most?

Late payments (35% of score), high credit utilization over 30%, collections, and bankruptcies.