A budget is the single most powerful tool for building wealth. It tells every dollar where to go before the month begins, so you never wonder where your money went. This guide is for you whether you are new to budgeting or have tried and quit. It covers six clear steps to create a monthly budget.

Why You Need a Monthly Budget

Without a budget, spending is based on feelings, not facts. Studies show that people without budgets consistently underestimate their spending by 20–30%. A budget gives you:

- Visibility — Know exactly where every dollar goes.

- Control — Stop money from disappearing on impulse purchases.

- Progress — Track savings goals, debt payoff, and net worth growth.

- Reduced stress — Bills are covered, emergencies are planned for.

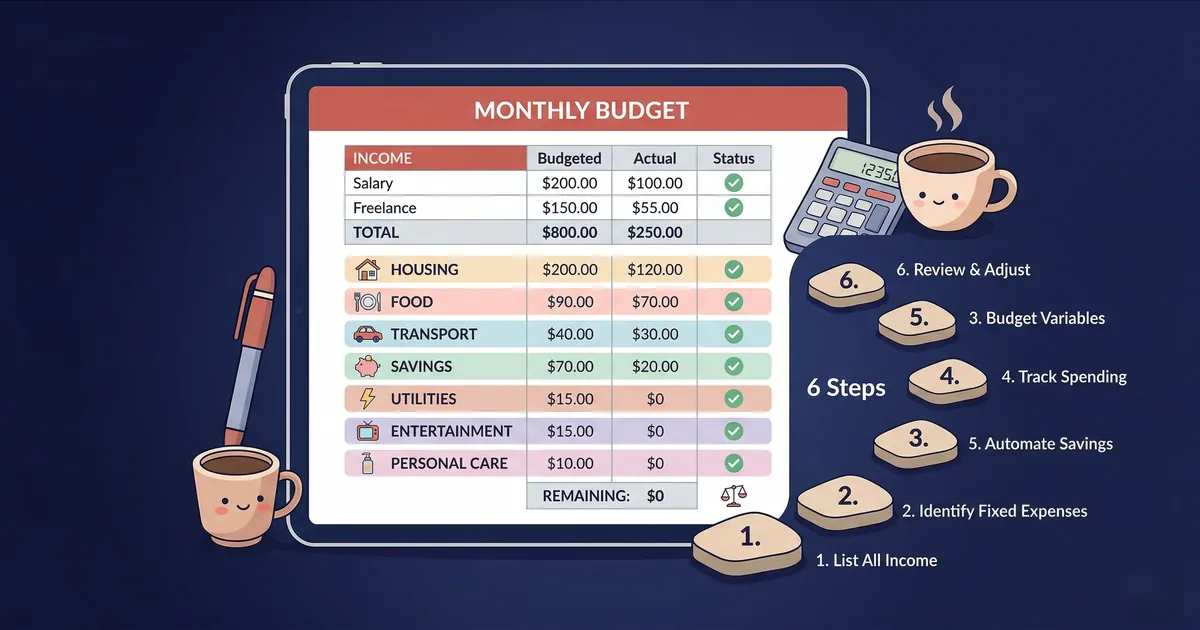

6 Steps to Create Your Monthly Budget

Step 1: Calculate Your Monthly Income

Write down your total take-home pay (after taxes and deductions). Include all income sources: salary, side hustle, freelance, rental income, and any regular transfers.

Step 2: List All Monthly Expenses

Review the last 2–3 months of bank and credit card statements. Write down every expense, no matter how small. Group them into categories:

- Fixed expenses: Rent/mortgage, car payment, insurance, subscriptions.

- Variable expenses: Groceries, gas, utilities, dining out.

- Periodic expenses: Car maintenance, annual subscriptions, gifts.

Step 3: Set Your Financial Goals

What do you want your money to do? Common goals include:

- Build a $1,000 emergency fund.

- Pay off $5,000 in credit card debt in 12 months.

- Save $300/month for a vacation.

- Contribute 15% to retirement.

Rank your goals by priority. Your budget should reflect these priorities.

Step 4: Assign Every Dollar a Job

Subtract your expenses and goals from your income. The result should be zero — every dollar is either spent on needs, wants, savings, or debt. This approach is called zero-based budgeting. It ensures no money goes untracked. If you have money left over, increase savings or debt payments. If you are short, cut wants or reduce variable expenses.

Step 5: Track Your Spending

A budget only works if you monitor it. Choose a tracking method:

- App: Use Budgeting365 to log expenses in seconds.

- Spreadsheet: Build a simple sheet with categories and running totals.

- Pen and paper: Write down every purchase daily.

The method matters less than consistency. Track every day for the first month.

Step 6: Review and Adjust Monthly

At the end of each month, compare your actual spending to your plan. Ask:

- Which categories did I overspend?

- Which categories had money left over?

- Did I hit my savings/debt goals?

- What needs to change next month?

Adjust your budget each month. It takes 2–3 months to find what works for you.

Budget Categories Breakdown

Here is a sample budget for a household earning $4,500/month after taxes:

| Category | Amount | % of Income |

|---|---|---|

| Housing (rent/mortgage) | $1,350 | 30% |

| Groceries | $450 | 10% |

| Transportation | $360 | 8% |

| Utilities | $225 | 5% |

| Insurance | $270 | 6% |

| Savings | $450 | 10% |

| Debt Repayment | $450 | 10% |

| Entertainment | $225 | 5% |

| Dining Out | $180 | 4% |

| Personal Care | $135 | 3% |

| Subscriptions | $90 | 2% |

| Clothing | $90 | 2% |

| Sinking Funds | $225 | 5% |

| Total | $4,500 | 100% |

Choose a Budgeting Method

| Method | Best For | How It Works |

|---|---|---|

| 50/30/20 | Beginners | 50% needs, 30% wants, 20% savings/debt |

| Zero-Based | Detail-oriented people | Every dollar assigned until income minus expenses equals zero |

| Envelope | Overspenders | Cash in physical or digital envelopes per category |

| Pay Yourself First | Savers | Save first, then spend the rest freely |

Common Budgeting Mistakes

- Making it too restrictive: Cut fun too aggressively and you will quit. Include some wants.

- Forgetting irregular expenses: Annual bills, car repairs, and gifts will blow your budget if unplanned. Use sinking funds to save for these in advance.

- Not tracking daily: The first month requires daily tracking. It takes 5 minutes.

- Giving up after one bad month: Every budgeter has bad months. Adjust and keep going.

- Not adjusting: Life changes. Your budget should change with it.

Start Your Budget Today

Budgeting365 makes it easy to set up categories, track expenses, and visualize your spending — all free, offline, and encrypted.

Download Budgeting365 — FreeFrequently Asked Questions

How much should I budget for each category?

Start with the 50/30/20 rule: 50% needs, 30% wants, 20% savings and debt. Adjust based on your income, cost of living, and goals. Understanding the difference between needs and wants is key.

What is the best budgeting method for beginners?

The 50/30/20 budget is simplest because it only uses three categories. Graduate to zero-based budgeting when you want more control.

How often should I review my budget?

Weekly for the first 2–3 months, then monthly once the habit is established. Always review after major life changes.

What if my income varies each month?

Budget based on your lowest expected monthly income. When you earn more, add the extra to savings or debt. See our full guide on budgeting with irregular income.

Should I include irregular expenses in my budget?

Yes. Create a sinking fund: divide annual costs by 12 and set aside that amount monthly so irregular expenses are always covered.