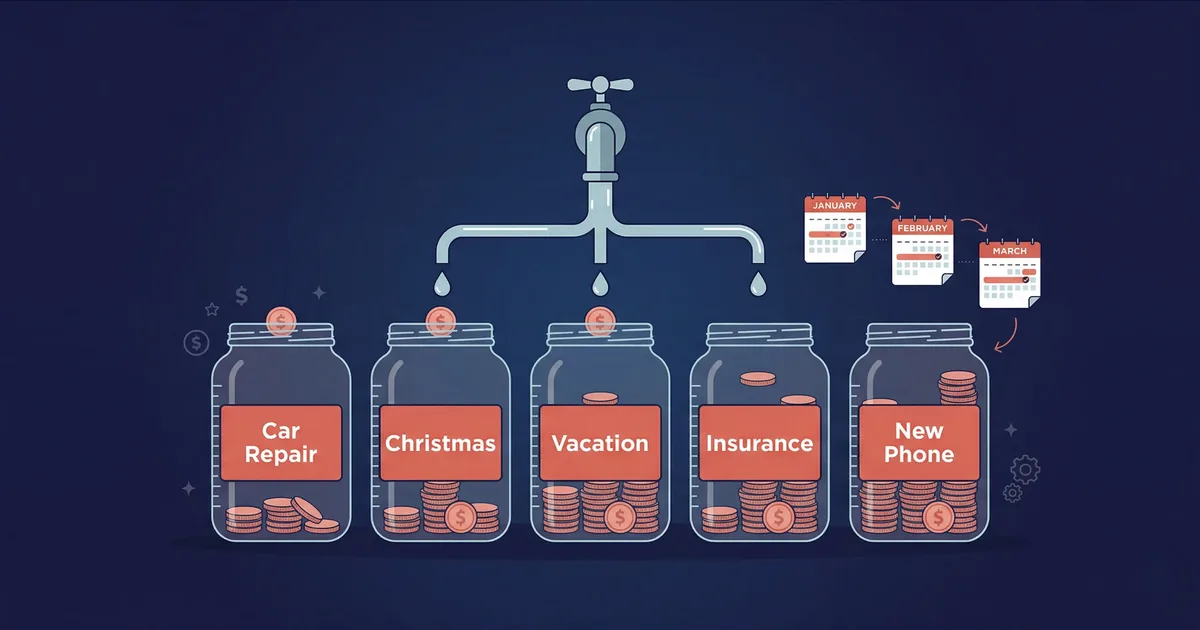

Have you ever been surprised by an expense you should have planned for? Holiday gifts, car registration, annual insurance premiums — these aren’t emergencies. They’re predictable. Sinking funds turn these expensive surprises into easy monthly savings.

What Are Sinking Funds?

Example: You spend $600 on holiday gifts each December. Instead of rushing in December, save $50/month starting in January. By December, you have $600 ready — no debt, no stress.

Sinking Funds vs. Emergency Fund

| Feature | Sinking Fund | Emergency Fund |

|---|---|---|

| Purpose | Planned, expected expenses | Unexpected emergencies |

| Examples | Holidays, car repairs, vacation | Job loss, medical emergency |

| Timeline | Specific date or season | Unknown — whenever needed |

| Amount | Known or estimated | 3–6 months of expenses |

| Replenish? | Refill after each use | Rebuild after each withdrawal |

Essential Sinking Fund Categories

| Category | Annual Cost | Monthly Savings |

|---|---|---|

| Holiday gifts | $600 | $50 |

| Car maintenance | $1,200 | $100 |

| Medical/dental copays | $600 | $50 |

| Home repairs | $2,400 | $200 |

| Annual subscriptions | $360 | $30 |

| Vacation | $2,000 | $167 |

| Clothing/shoes | $600 | $50 |

| Car insurance (annual) | $1,200 | $100 |

| Back to school | $300 | $25 |

| Pet care | $500 | $42 |

Total: $9,760/year or $814/month across all categories. Most families start with 3–5 and add more over time.

How to Calculate Your Amounts

- List every irregular expense you’ve paid in the last 12 months (check bank statements)

- Estimate annual cost for each expense

- Divide by months remaining until the expense is due

- Set up monthly auto-transfers into your sinking fund account

Setting Up Your Sinking Funds (5 Steps)

- Audit irregular expenses: Pull 12 months of bank/credit card statements. List every non-monthly expense.

- Prioritize categories: Rank by urgency (nearest deadline first) and consequence (what hurts most if unprepared).

- Choose your tracking method: Separate savings accounts, a spreadsheet, or a budgeting app like Budgeting365 with named categories.

- Automate contributions: Set up automatic transfers on payday. Even $10–$20 per category adds up over 12 months.

- Review quarterly: Adjust amounts based on actual spending. Add new categories as needed.

Starter Kit: 5 Must-Have Sinking Funds

- Car maintenance: Oil changes, tires, brakes, registration ($100/mo)

- Holiday gifts: Christmas, birthdays, anniversaries ($50–$100/mo)

- Medical: Copays, prescriptions, dental cleanings ($50/mo)

- Home repairs: Even renters need this for deposits, appliance replacement ($50–$200/mo)

- Annual bills: Insurance, subscriptions, memberships ($30–$100/mo)

Track Sinking Funds in Budgeting365

Create named savings categories, set targets, and watch progress bars fill up toward every goal — free, offline, AES-256 encrypted.

Download Budgeting365 — FreeFrequently Asked Questions

What is a sinking fund?

Money saved monthly for a planned future expense. It turns irregular costs into manageable monthly savings.

How is a sinking fund different from an emergency fund?

Emergency funds cover unexpected events. Sinking funds cover expected but irregular expenses like holidays and car maintenance.

How many sinking funds should I have?

Start with 3–5 essential categories. Most people find 5–8 ideal. Too many becomes hard to manage.

Where should I keep sinking fund money?

A high-yield savings account. Track sub-categories with a budgeting app or separate accounts.

What if I can’t afford to fund all categories?

Prioritize by urgency. Even $10–$20/month per category is better than nothing. Increase contributions as income grows.