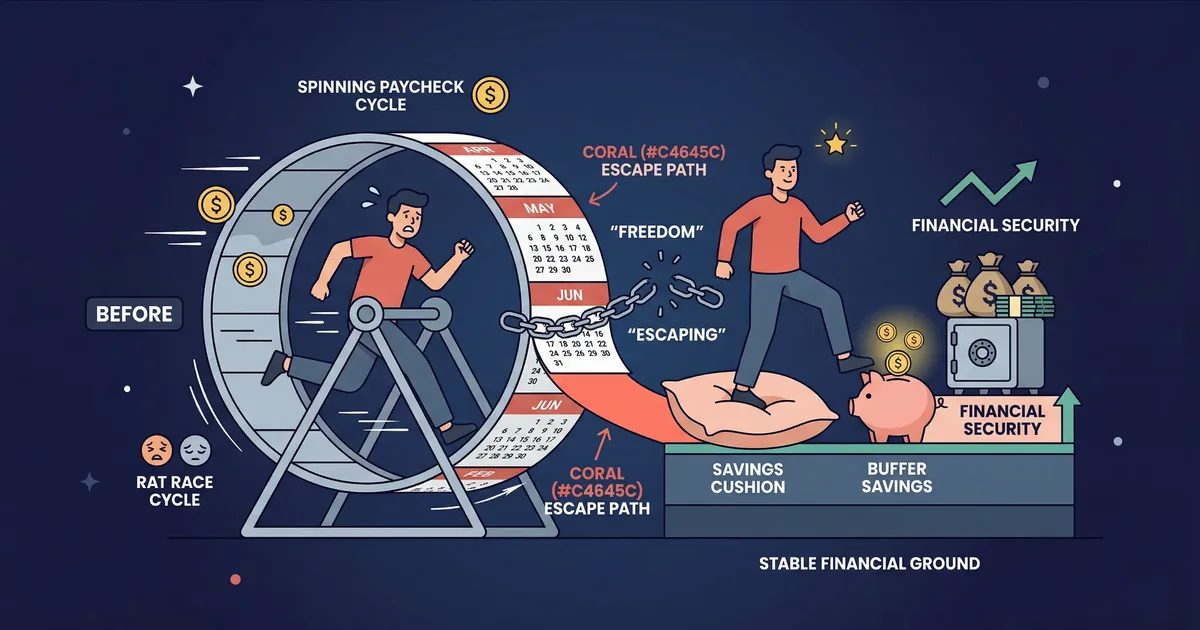

About 60% of Americans live paycheck to paycheck — and many earn much more than the average salary. If your bank account drops close to zero before each payday, you are not alone. But you can break the cycle with a clear plan.

The Paycheck-to-Paycheck Reality

Living paycheck to paycheck means having little to no money left after paying monthly expenses. According to a CNBC/LendingClub report, roughly 60–65% of Americans experience this, including many six-figure earners. One unexpected bill can cause a money emergency. You may have to rely on credit cards, payday loans, or borrowed money.

Diagnose the Problem

Before you can fix the cycle, identify what is causing it:

| Root Cause | Signs | First Action |

|---|---|---|

| No budget | No idea where money goes | Track every dollar for 30 days |

| Lifestyle inflation | Income rose but savings didn’t | Freeze spending at current level |

| Too much debt | Large monthly debt payments | List all debts with balances and rates |

| Income too low | Basic needs use up 90%+ of pay | Explore income-boosting options |

| Irregular expenses | Surprise bills each month | Set up monthly sinking funds for yearly expenses |

The 6-Step Escape Plan

Step 1: Track Every Dollar for 30 Days

Write down or use an app to record every expense for one full month. Categorize spending into needs (housing, food, transport, insurance) and wants (dining out, entertainment, subscriptions, shopping).

Step 2: Cut the Fat

Review your 30-day spending and eliminate or reduce:

| Cut | Monthly Savings | Annual Impact |

|---|---|---|

| Unused subscriptions | $30–$80 | $360–$960 |

| Reduce dining out by half | $100–$250 | $1,200–$3,000 |

| Switch to cheaper phone plan | $20–$50 | $240–$600 |

| Brew coffee at home | $60–$120 | $720–$1,440 |

| Cancel gym (workout at home) | $30–$60 | $360–$720 |

| Negotiate insurance rates | $25–$75 | $300–$900 |

| Potential total | $265–$635 | $3,180–$7,620 |

Step 3: Build a $1,000 Emergency Starter Fund

This is your first milestone. With even a small buffer, you stop relying on credit for unexpected expenses. Sell items, pick up extra shifts, or redirect every freed-up dollar until you hit $1,000.

Step 4: Build a One-Month Buffer

What really helps is having next month’s expenses saved ahead of time. When you are living on last month’s income, you are no longer paycheck to paycheck.

Step 5: Attack High-Interest Debt

Debt payments reduce the money you have available each month. Use the avalanche method (highest interest first) or snowball method (smallest balance first) to systematically eliminate debt and free up money.

Step 6: Increase Your Income

- Ask for a raise (research shows only 37% of workers ever ask)

- Start a side hustle: freelancing, tutoring, delivery driving, selling handmade goods

- Sell unused items: furniture, electronics, clothing, collectibles

- Develop skills for a higher-paying role

- Work overtime or pick up extra shifts when available

Realistic Timeline

| Milestone | Timeline | How |

|---|---|---|

| Track all spending | Month 1 | App or notebook tracking |

| Cut $200+/month in expenses | Month 1–2 | Cancel, negotiate, reduce |

| Save $1,000 emergency fund | Month 2–4 | Redirect freed cash + sell items |

| Build one-month buffer | Month 4–8 | Save consistently from cuts + income |

| Pay off high-interest debt | Month 6–18 | Snowball or avalanche method |

| Full 3-month emergency fund | Year 1–2 | Redirect former debt payments |

Start Breaking the Cycle Today

Budgeting365 helps you track every dollar, see where your money goes, and build toward financial freedom — free and offline.

Download Budgeting365 — FreeFrequently Asked Questions

What percentage of people live paycheck to paycheck?

About 60–65% of Americans, including many six-figure earners. It is a cash flow and planning problem, not just an income problem.

How long does it take to break the cycle?

Most people can build a one-month buffer in 3–6 months. Full stability (3–6 month emergency fund) typically takes 1–2 years.

What is the fastest way to build a buffer?

Sell unused items, cut your 3 largest variable expenses, take on extra work, and save every freed dollar into a separate account.

Should I pay off debt or save first?

Build a $1,000 starter emergency fund first, then attack high-interest debt while maintaining that buffer.

Can I break the cycle on a low income?

Yes, though it takes longer. Start small ($25/week), eliminate one subscription, negotiate one bill, and look for ways to boost income.