If you have ever searched for “how to budget” you have probably seen the 50/30/20 budget rule. It is the most popular budgeting framework for a reason: it is simple, flexible, and works for almost any income level. Instead of tracking every cent across dozens of categories, you split your take-home pay into just three buckets — needs, wants, and savings.

In this guide we will explain how the 50/30/20 rule works and walk through a real-money example. We will also show you when to adjust the percentages and how to track it all with a free budget tracker app.

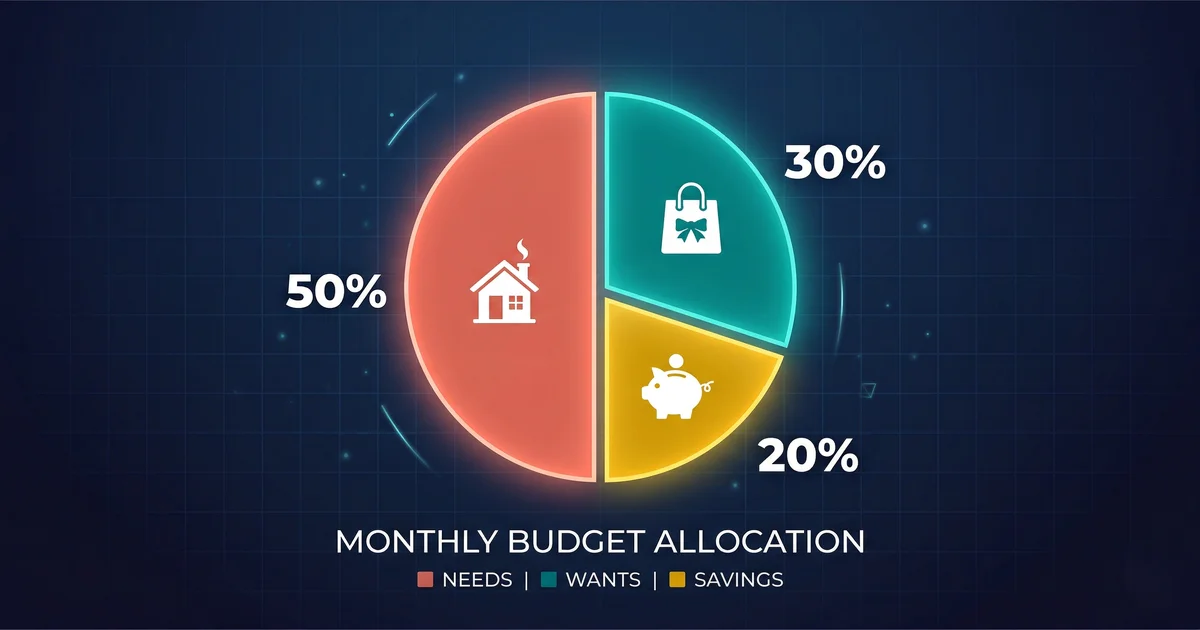

What Is the 50/30/20 Budget Rule?

The 50/30/20 rule was popularized by Senator Elizabeth Warren and her daughter Amelia Warren Tyagi in their 2005 book All Your Worth: The Ultimate Lifetime Money Plan. The core idea is simple:

30% of after-tax income → Wants (non-essentials you enjoy)

20% of after-tax income → Savings & Debt (building your future)

The beauty of this budgeting method is its simplicity. You do not need a finance degree or complicated spreadsheets. You just need to know your take-home pay and be honest about which expenses are true needs versus wants.

How the 50/30/20 Rule Works (Step by Step)

Step 1: Calculate Your After-Tax Income

Start with the money that actually hits your bank account each month. If you are a salaried employee, this is your net pay after taxes, Social Security, and Medicare are deducted. If you are self-employed, subtract your estimated tax payments from your gross income.

Include all reliable income sources: your primary salary, side-hustle income, freelance payments, and any regular investment income. Do not include one-time payments like bonuses or tax refunds — treat those as extra money toward savings.

Step 2: Multiply to Find Your Targets

Once you know your monthly take-home pay, the math is straightforward:

| Category | Percentage | Formula |

|---|---|---|

| Needs | 50% | Take-home pay × 0.50 |

| Wants | 30% | Take-home pay × 0.30 |

| Savings & Debt | 20% | Take-home pay × 0.20 |

Step 3: Categorize Every Expense

Go through your bank and credit card statements from the past month. Assign each transaction to one of the three buckets. For more detailed tracking methods, see our guide on how to track expenses. This is where most people find surprises — that “essential” streaming subscription? That is a want. The basic phone plan? That is a need. A premium unlimited plan? The base cost is a need; the upgrade portion is a want.

Step 4: Compare and Adjust

Compare your actual spending to the 50/30/20 targets. If your needs exceed 50%, look for ways to reduce fixed costs — refinance loans, switch insurance providers, or downsize housing. If your wants are over 30%, identify subscriptions or habits you can cut. The goal is not perfection on day one; it is gradual improvement month over month.

What Counts as Needs vs. Wants

The hardest part of the 50/30/20 rule is being honest with yourself about what is a need and what is a want. Here is a clear breakdown:

Needs (50%) — Must-Pay Expenses

- Housing: Rent or mortgage payment

- Groceries: Basic food and household supplies

- Utilities: Electricity, water, gas, basic internet

- Transportation: Car payment, fuel, public transit pass

- Insurance: Health, auto, renters/homeowners insurance

- Minimum debt payments: Student loans, credit card minimums

- Childcare: Daycare or after-school care

- Healthcare: Prescriptions, copays, essential medical costs

Wants (30%) — Nice-to-Have Expenses

- Dining out: Restaurants, coffee shops, takeout

- Entertainment: Streaming services, concerts, movies

- Shopping: Clothing beyond basics, electronics, gadgets

- Hobbies: Gym memberships, sports equipment, crafts

- Travel: Vacations, weekend trips

- Subscriptions: Music, gaming, magazine subscriptions

- Upgrades: Premium phone plan, luxury groceries, brand-name items

Savings & Debt Repayment (20%)

- Emergency fund: Build 3–6 months of expenses

- Retirement: 401(k) contributions, IRA, pension

- Extra debt payments: Paying above minimums on loans or credit cards

- Investments: Stocks, bonds, index funds, savings accounts

- Savings goals: Down payment fund, car fund, education fund

Pro tip: If your employer matches 401(k) contributions, always contribute at least enough to get the full match. That is free money and should be your first savings priority.

50/30/20 Budget Example ($4,000/Month)

Let us walk through a real example. Say your monthly take-home pay is $4,000:

| Category | Target | Budget Amount | Example Expenses |

|---|---|---|---|

| Needs | 50% | $2,000 | Rent $1,200 + Groceries $350 + Utilities $150 + Car $200 + Insurance $100 |

| Wants | 30% | $1,200 | Dining $250 + Entertainment $100 + Shopping $200 + Gym $50 + Travel $400 + Subscriptions $200 |

| Savings | 20% | $800 | Emergency fund $300 + Retirement $300 + Extra debt payment $200 |

In this example the person allocates $2,000 to essentials, $1,200 to enjoyment, and $800 toward financial security. If followed consistently, that $800/month in savings adds up to $9,600 per year. That is enough to build a solid emergency fund in under a year and start investing after that.

When to Adjust the 50/30/20 Percentages

The 50/30/20 split is a starting guideline, not a rigid law. Here are common situations where you might adjust:

High Cost of Living Areas

If you live in an expensive city, rent alone may take 40% of your income. A 60/20/20 or even 70/20/10 split may be more realistic. The key is to still set aside something for savings every month, even if it is a smaller percentage.

Aggressive Savings Goals

If you are saving for a house down payment or aiming for early retirement, try switching things around. Use a 50/20/30 split where 30% goes to savings. Some “FIRE” (Financial Independence, Retire Early) practitioners save 50% or more of their income.

Debt-Heavy Situations

If you are carrying high-interest credit card debt, temporarily shift your budget to a 50/20/30 split. The extra 10% from wants goes toward faster debt repayment. Once your high-interest debt is cleared, return to the standard 50/30/20.

Low Income

If your essential expenses already exceed 50% of your income, do not feel defeated. Start with whatever split reflects your reality — even 70/20/10 is a plan. Planning where your money goes is more important than hitting exact percentages.

Alternative Budgeting Methods

| Method | Split | Best For |

|---|---|---|

| 50/30/20 (Standard) | 50/30/20 | Most people — balanced approach |

| 60/20/20 | 60/20/20 | High cost of living areas |

| 80/20 | 80/20 | Simplest — save 20%, spend the rest |

| 70/20/10 | 70/20/10 | Lower incomes or heavy debt |

| 50/20/30 (Saver) | 50/20/30 | Aggressive savings goals |

How to Track Your 50/30/20 Budget

Knowing the percentages is one thing — actually tracking them is another. Here is how to put the 50/30/20 rule into practice:

1. Set Up Three Budget Categories

In your budget tracker app, create three main categories: Needs, Wants, and Savings. Set the budget limits based on your income split. With Budgeting365, you can create custom budget categories with visual progress rings. These show exactly how much you have left in each bucket.

2. Log Expenses Daily

The key to any budgeting method is consistency. Spend two minutes each evening logging your transactions. Most people find that the act of recording a purchase makes them more conscious about spending.

3. Review Weekly

Check your progress every Sunday. Are you on track in each category? If your “wants” spending is going up mid-month, you still have time to adjust for the remaining weeks.

4. Adjust Monthly

At the end of each month, review how your actual spending compared to your targets. Did an unexpected car repair push your “needs” over? That is fine — adjust next month. Did you save more than 20%? Celebrate the win and consider investing the extra.

Start Tracking Your Budget Today

Budgeting365 makes the 50/30/20 rule easy with custom categories, visual progress tracking, and complete offline privacy.

Download Budgeting365 — FreeFrequently Asked Questions

What is the 50/30/20 budget rule?

The 50/30/20 budget rule is a simple framework that divides your after-tax income into three categories: 50% for needs (rent, groceries, utilities), 30% for wants (dining, entertainment, subscriptions), and 20% for savings and debt repayment. It was popularized by Senator Elizabeth Warren in her book All Your Worth.

Who invented the 50/30/20 rule?

Senator Elizabeth Warren and her daughter Amelia Warren Tyagi introduced the rule in their 2005 book All Your Worth: The Ultimate Lifetime Money Plan. It has since become one of the most widely recommended budgeting methods by financial advisors worldwide.

Is the 50/30/20 rule good for low income?

The percentages can be adjusted for lower incomes. If your needs exceed 50%, try a 60/20/20 or 70/20/10 split. The important principle is to always allocate something toward savings, even if it is a smaller percentage. Any conscious budget plan is better than none.

How do I track my 50/30/20 budget?

Use a budget tracking app like Budgeting365 to create three budget categories matching your 50/30/20 targets. Log transactions daily and review your visual progress weekly to stay on track.

What counts as needs vs. wants in the 50/30/20 rule?

Needs are essential expenses: rent, groceries, utilities, insurance, minimum debt payments, and basic transportation. Wants are non-essential expenses that improve quality of life: dining out, streaming services, hobbies, vacations, and upgrades beyond basic needs.