With tap-to-pay and digital wallets everywhere, cash budgeting may sound old-fashioned. But the data is clear: people spend 12–18% less with physical cash. If you keep overspending no matter what app you use, the cash envelope method could be the fresh start you need.

Why Cash Budgets Work

- Built-in spending limit: When the envelope is empty, you stop spending. No overdrafts, no credit card debt.

- Visual accountability: You can see and feel how much money is left this week

- No transaction fees: Cash is free to use everywhere

- Privacy: Cash leaves no digital trail — no tracking, no data harvesting

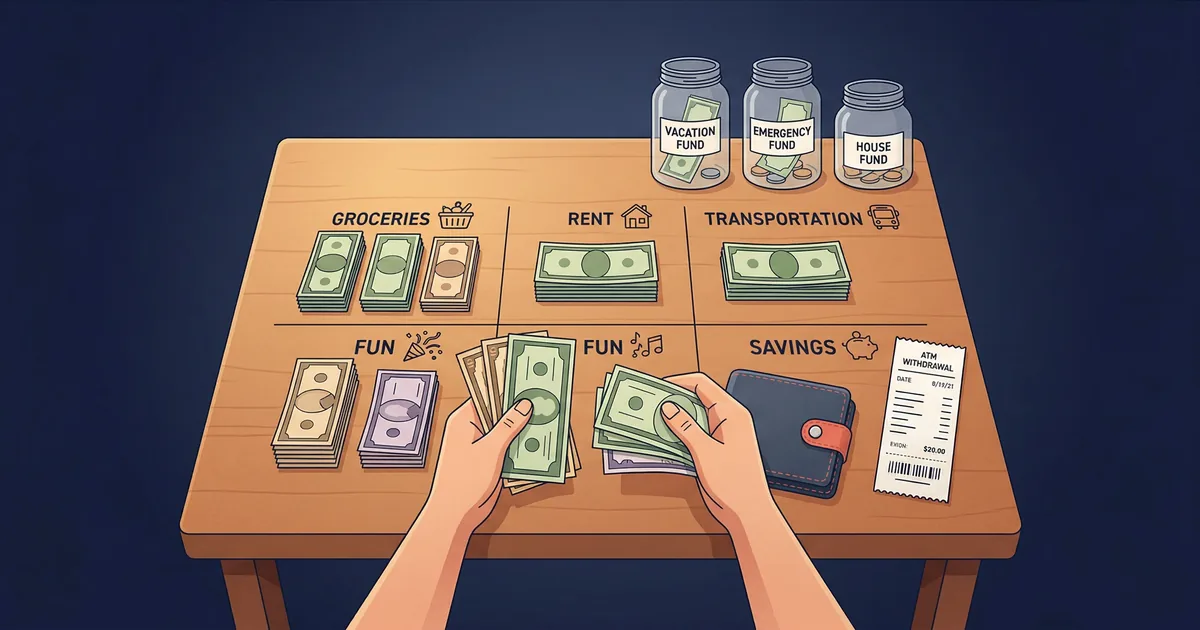

Best Categories for Cash Envelopes

| Use Cash For | Keep on Autopay |

|---|---|

| Groceries | Rent / Mortgage |

| Dining out | Utilities |

| Gas / transportation | Insurance premiums |

| Entertainment | Phone / internet |

| Personal care | Subscriptions |

| Clothing | Loan payments |

| Miscellaneous | Savings transfers |

Use cash for variable spending (categories where you tend to overspend). Keep fixed bills on autopay so you never miss a payment.

How to Set Up Cash Envelopes

Step 1: List Your Cash Categories

Choose 4–6 spending categories where you overspend the most. Fewer envelopes = simpler system.

Step 2: Set Monthly Limits

Look at two months of spending to see what you actually spend per category. Then set a slightly lower target. Be realistic — extreme cuts do not last.

Step 3: Withdraw Cash on Payday

Go to the bank or ATM and withdraw the total amount for all envelopes. Divide it immediately.

Step 4: Label & Stuff Envelopes

Write the category name and monthly limit on each envelope. Put the assigned amount inside. Store them in a secure binder or wallet at home.

Step 5: Spend Only from Envelopes

Going grocery shopping? Grab the grocery envelope. Meeting friends for dinner? Bring the dining-out envelope. When an envelope is empty, that category is done for the month.

Sample Cash Budget ($1,250/mo Variable Spending)

| Envelope | Monthly | Weekly |

|---|---|---|

| Groceries | $400 | $100 |

| Dining out | $200 | $50 |

| Gas | $250 | $63 |

| Entertainment | $150 | $38 |

| Personal care | $100 | $25 |

| Miscellaneous | $150 | $38 |

| Total | $1,250 | $314 |

Pro Tips for Cash Budgeting

- Withdraw weekly, not monthly: Carrying $1,250 is risky. Split into four weekly withdrawals for safety.

- Keep a small “buffer” envelope: $50–$100 for unexpected small expenses

- Use a spending tracker app: Even with cash, log expenses in Budgeting365 so you have a record

- Borrow between envelopes carefully: If dining runs out, you can borrow from entertainment — but never from savings

- Save loose change: Empty your pockets daily into a coin jar. Most people save $200–$400/year this way

- Review weekly: Check envelopes every Sunday to see where you stand

Track Cash Spending Digitally

Use Budgeting365 alongside cash envelopes to log every expense, see category breakdowns, and stay organized — even offline.

Download Budgeting365 — FreeFrequently Asked Questions

Is cash better than a debit card?

For variable spending categories, yes. Studies show people spend 12–18% less with cash.

How do I handle online purchases?

Use a separate prepaid card or checking account with a fixed monthly limit. Move the same amount of cash from that envelope to stay on track.

What about leftover cash at month-end?

Add it to next month, move it to savings, or share it with envelopes that ran short.

Is carrying cash safe?

Withdraw weekly instead of monthly to minimize risk. Only carry what you need for the week.

How many envelopes should I have?

Start with 4–6 covering your highest variable spending categories. Add more later if needed.